Stamps Printed by Thomas de la Rue Ltd in Great Britain

from 1869 Onwards

Internal Revenue

Stamps

As with Bills of Exchange stamps, these were first introduced in 1869. There were, however, no locally-printed issues involved, the first coming from De La Rue. Prior to these arriving from Britain, it appears that postage stamps may have b een used for internal revenue purposes. There are eight such stamps listed on page 82 of Morley's 1910 catalogue, where he states "This set is catalogued by Moens, but no copies can be traced". Barefoot does not include them, and I have never seen the Moens listing. Neither have I ever seen a stamp with an obvious fiscal cancel from these Victorian issues. One must assume that copies are extremely rare that they just do not exist.

Governments found Internal Revenue stamps a very

convenient form of tax collection, with administrative costs being kept

to the minimum. They were used for a variety of purposes. Some of these

are listed below, although this list is not necessarily exhaustive.

Where known, Sterling price of the stamp required is shown in brackets

after the heading. In cases where no value is shown, ad valorum duty was

paid in most cases.

BILL OF LADING

This is a legal document between a shipper of a particular commodity and

the carrier detailing the type of goods, the quantity and the

destination. It also serves as a receipt of the shipment when the goods

are delivered to the prescribed destination.

PATENTS FOR INVENTIONS

Such a document would convey upon the patentee the exclusive right to

prevent others from making, using or selling and distributing the

patented invention without permission.

DEBENTURE AND SHARE CERTIFICATES

A debenture is normally issued by a company, in the form of a

certificate of indebtedness by the company, to the owner of the debt. It

will often contain express provisions regarding the payment of interest

and the date on which the debt is to be repaid. Usually, a debenture can

be transferred from one owner to another. A share certificate recognises

that the holder owns a share of a company. Again, this is transferable

from one owner to another.

CHARTER PARTY (Two shillings)

This is a contract between the owner of a vessel and the charterer for

the use of a vessel. The charterer takes over the vessel for either a

certain amount of time (a time charter) or for a certain point-to-point

voyage (a voyage charter). These are the two main types of charter. The

phrase “Charter Party” is derived from the Latin charter partite, a

legal paper or instrument divided i.e. written in duplicate so that each

party retains half.

DOCK WARRANT (Four shillings)

In law, this is a document by which the owner of a marine or river dock

certifies that the holder is entitled to goods imported and warehoused

in the docks.

PASSPORT (Four shillings)

As everyone knows, this is a document to enable free passage from one

country to another. What is not so well-known is that some which were

produced in earlier times, including those in Mauritius, required a

Revenue stamp affixed as evidence of the duty paid to obtain the

passport in the first place.

OATH OF NATURALISATION (One pound)

The description of this oath has various titles in different parts of

the world. It is now generally known as the Oath of Allegiance and

Pledge of Loyalty. A person cannot be registered or naturalised as a

citizen of certain countries unless he or she has made the relevant

citizenship oath and pledge at a citizenship ceremony.

SURVEY REPORT ON SHIPS ( One shilling)

Such a Report would usually be conducted by a qualified Marine Surveyor.

Typically, this would include the structure, machinery and equipment and

general condition of a vessel. It is often closely associated with

marine insurance.

BOTTOMRY BOND (Three shillings)

This is a type of merchant funding using a ship as security for a loan,

which may be needed to finance a voyage, to deal with urgent repairs or

for some other emergency. Their use declined during the nineteenth

century, and they are no longer utilised.

SECURITY BOND AGAINST A BREACH OF LAW (Five shillings)

This could arise where bail was given to an offender.

LEGALISATION OF SIGNATURE (Ten shillings)

This was done by Statutory Declaration to the Supreme Court of

Mauritius, if it was necessary to prove that a signature was genuine.

There are two examples of the type of document involved that are

described later in this section on Internal Revenue stamps.

FOREIGN BILL OF EXCHANGE

It is surprising to find this heading here, in view of the fact that

Bills of Exchange stamps were specifically designed for this purpose.

However, it is quite clear that Internal Revenue stamps were permitted

to be used, as will be seen later.

CERTIFICATE OF CLEARANCE

Such certificates were issued by the Mauritian Collector of Customs for

the clearance of ship's cargoes. An example is shown later in this

section.

Out of all the applications shown above, I have only seen Internal

Revenue stamps genuinely used on legalisation of signature documents ,

Bills of Exchange and Certificates of Clearance.

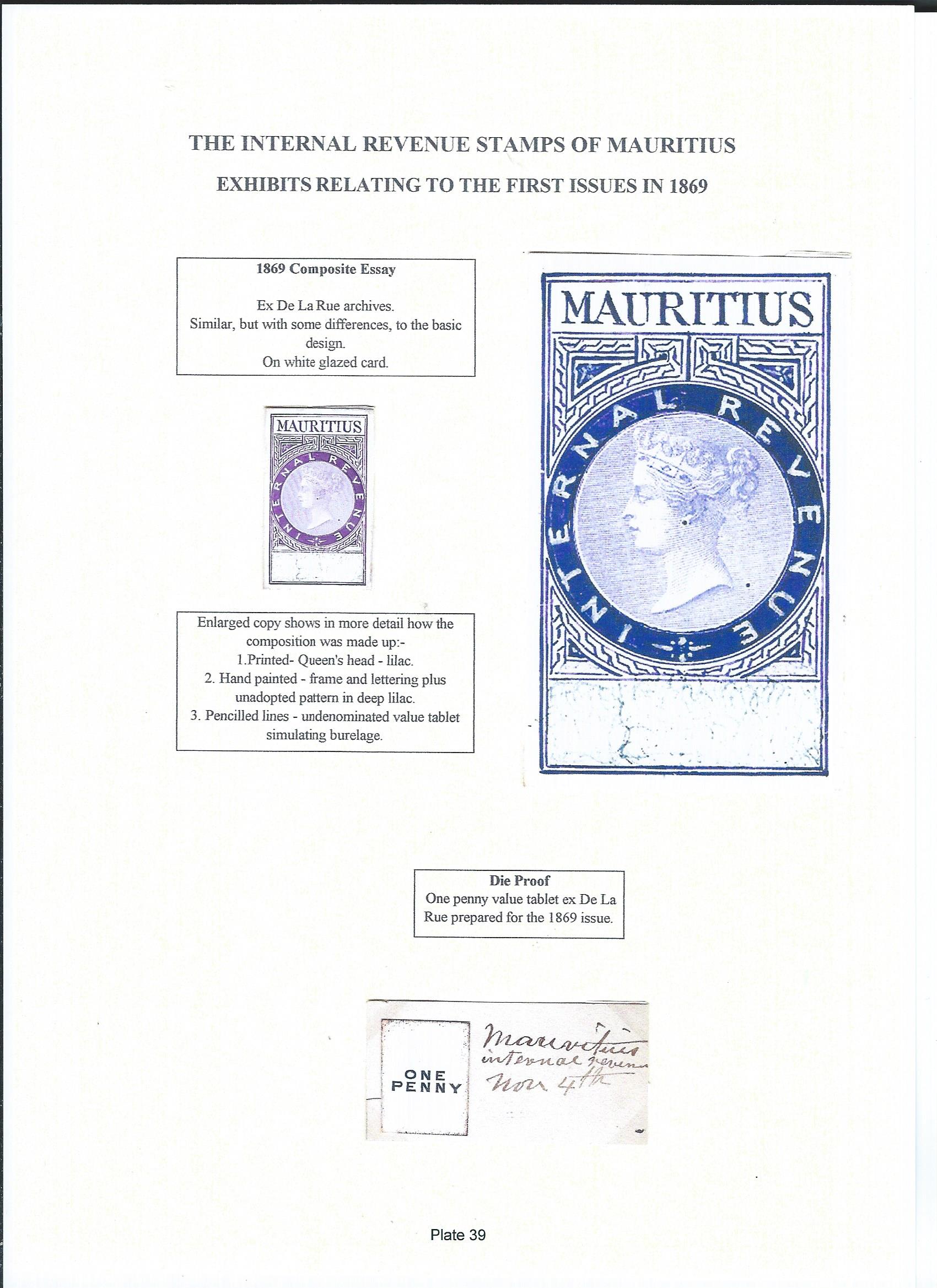

The first issue of Internal Revenue stamps in 1869/72 were, as usual,

preceded by De La Rue proofs. Two of these are shown on

Plate 39.

The first is a composite, partly hand-painted essay in an unadopted

purple shade. An enlargement of the original is also shown to indicate

the full details of the artist’s work. Everything is hand-drawn or

painted with the exception of Queen Victoria’s head. No value tablet has

been added because this would be separate die. The patterns were also

not adopted, and the value tablet has pencil “scribble” to simulate

burelage.This word is of French origin, and refers to an intricate

network of fine lines, dots or other designs printed over or as a

background of some stamps to prevent forgery.

Plate 39 (click to

enlarge)

An example of a die proof value tablet is also shown on the same plate.

This is for the one penny value and is printed in black, whereas the

finally-issued stamp shows the value in blue. The proof has been pasted

onto card, on which the words “Mauritius internal revenue Nov 4th”

appear in manuscript.

Plate 40 displays a number of more advanced proofs in

different forms. There are six proofs in total, and all show the final

design including the burelage which was only simulated on the previous

Plate. The first two stamps on the Plate are mounted on card without any

values being shown. They are mounted on black card, which appears to be

somewhat fugitive, because the colour overflows slightly onto the stamp

itself. They are both overprinted “SPECIMEN”- Samuel type D7. The next

four are on paper and are all in final colours of the values displayed.

The two pence blue and blue, the one pound mauve and brown and the five

shillings brown and purple are imperforate, but the two shillings is

perforated 14. All except the five shillings have the Samuel type D7

overprint.

Copies of the actual De La Rue issues of 1869/72 Internal Revenue stamps

are shown on Plates

41 and

42. Rather like the early

primitives, the mint items are much harder to obtain, and only two are

shown here - the one penny and the threepence. Apart from the one pound

issue, the others are rather dull productions and unlike the later, more

adventurous De La Rue attempts. This may, of course, have been

influenced by the Crown Agents for the Colonies who were the final

arbiters on design and colour.

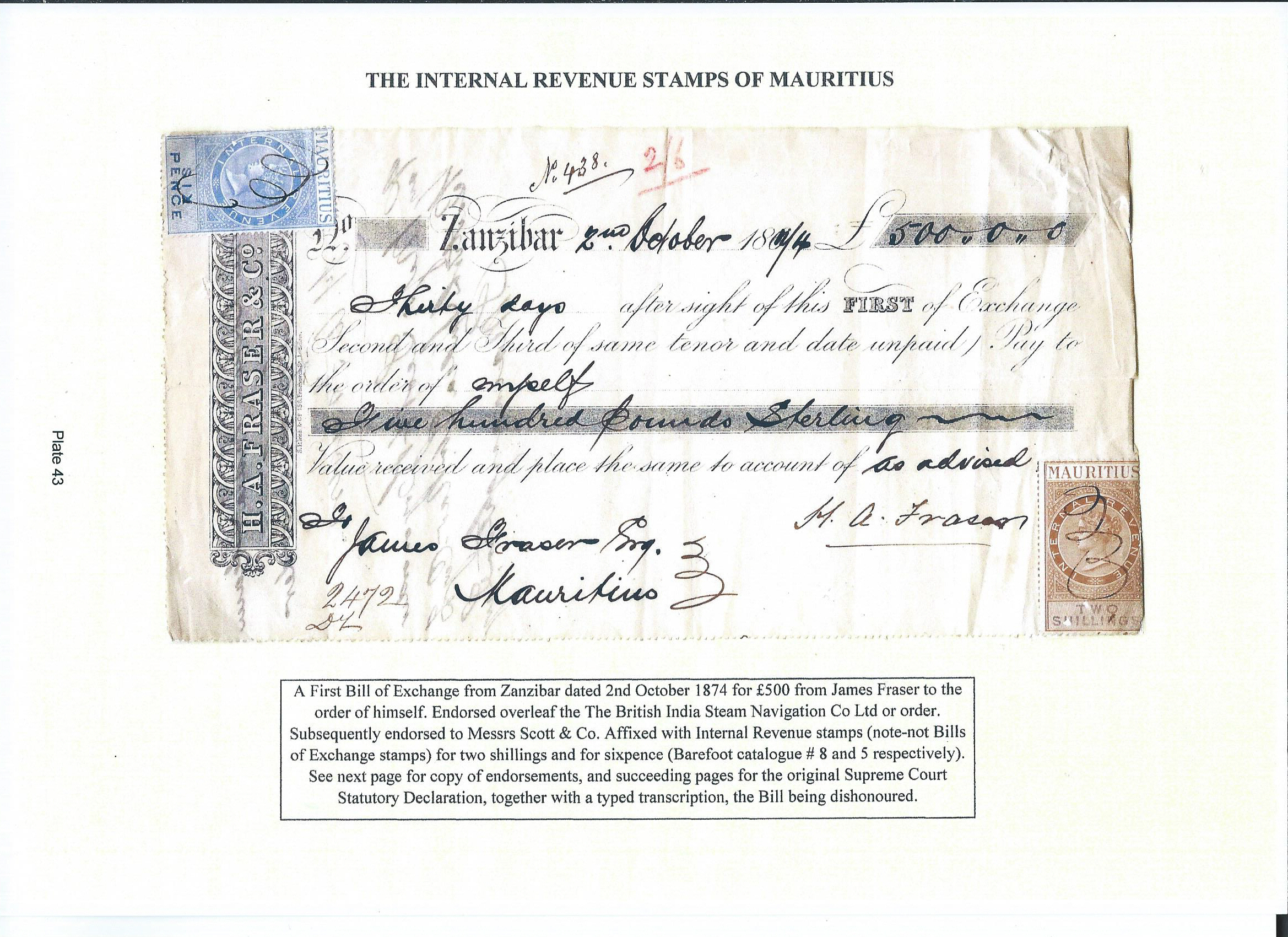

I mentioned earlier that Internal Revenue stamps are also permitted to

be used on Bills of Exchange. Plates

43 and

44 show an

example of this. The first Plate displays the front of the Bill which is

for £500 and is affixed with two Internal Revenue stamps for a total of

two shillings and sixpence. This is the correct tax charge for a Foreign

Bill of Exchange drawn in, but payable out of, Mauritius (see Plate 7

table of rates). the strange curly manuscript used to cancel the stamps

is also repeated against the drawer's name on the Bill itself.

Plate 43 (click to

enlarge)

The second Plate shows the reverse of the bill, and demonstrates why

such documents are termed "negotiable instruments" i.e. the rights for

ultimate encashment against James A Fraser can be passed by one

person/firm to another, usually for goods or cash payment (often

discounted). In this case, the Bill has been "negotiated" twice. On the

face of the Bill it was first written in favour of Fraser himself, but

it can be seen that he endorsed it on to the British India Steam

Navigation Co Ltd who subsequently endorsed it to Messrs Scott & Co.

However, the story does not end here, because

Plate 45

displays the top page of three containing a Supreme Court Statutory

Declaration. Very faintly at the top left of the document, is the

impression of a Supreme Court duty stamp for three pence. These

impressed duty stamps do not copy well, and are even quite difficult to

see in poor light on the original document. The impression is repeated

on each of the three sheets, making total duty of nine pence. I have

attempted to show a typed transcription on

Plate 46 as

the manuscript is difficult to read and, even then, I have been unable

to understand some words where I have used a question mark instead.

Briefly stated, the Declaration was made by the Court Usher, who visited

James A Fraser for the purpose of getting him the honour the Bill, which

he refused to do. The Declaration could subsequently be used by Scott &

Co as evidence if they wished to bring a Court action against Fraser.

This whole story is an interesting insight into some aspects of

commercial life at that time in history. It was difficult to know in

what section of the book I should introduce this tale but, in the end,

the Internal Revenue stamps won against Bills of Exchange and Impressed

Duty Stamps!

Apart from the elusive 10 rupees brown and purple issue, which is

actually shown on the document on

Plate 51, the rest of

the 1878/79 stamps are shown on

Plate 47. These are the

first of the new currency, when rupees and cents in decimal form

replaced pounds shillings and pence. Values are expressed in a mixture

of figures and words. Some shades are shown as well, but these are not

so markedly obvious in the printing reproduction. However, the rather

unadventurous colours of earlier stamps continue to be used.

De La Rue plate proofs comprise

Plate 48, when in 1879

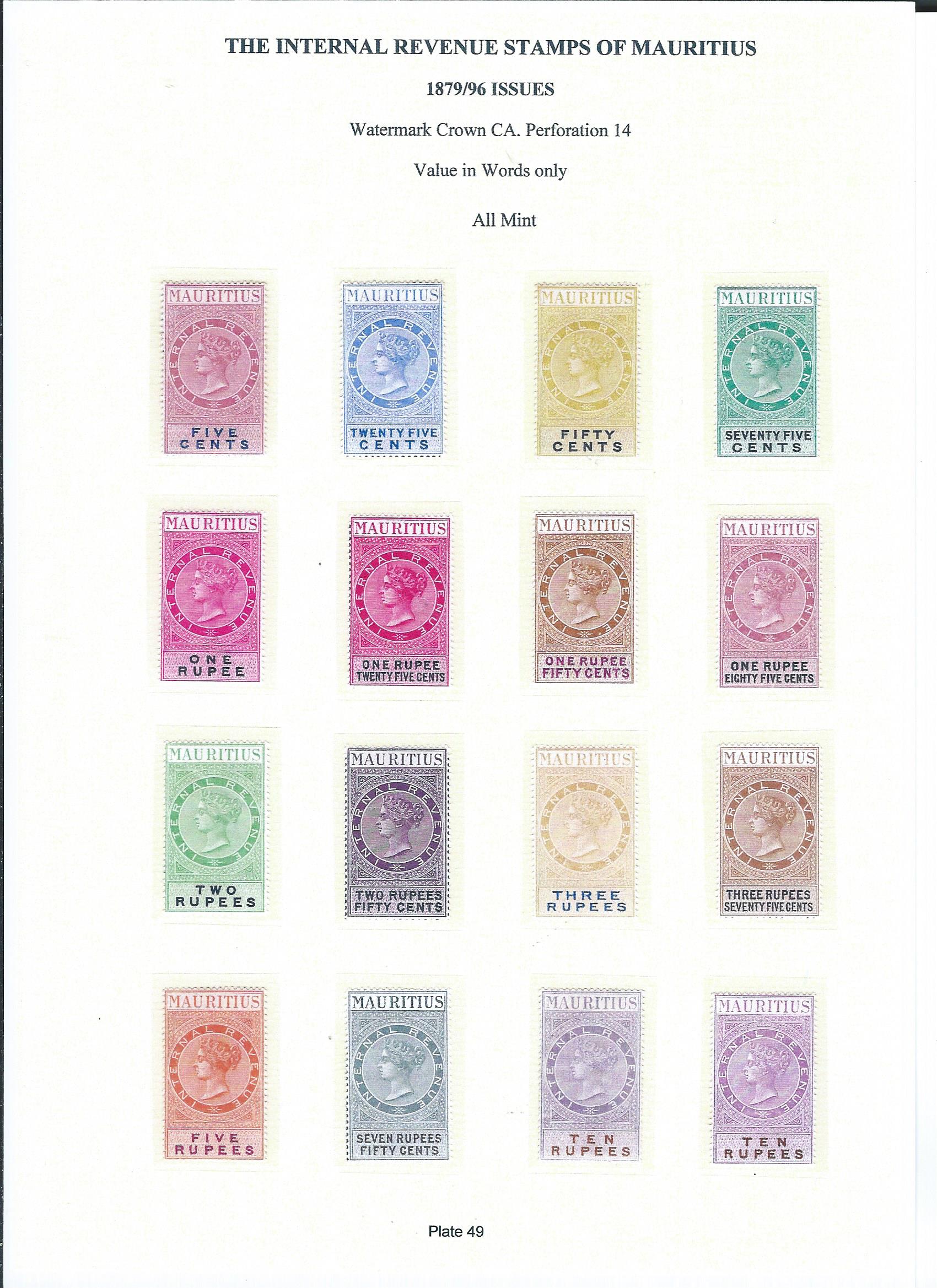

the values were changed to words only. Plates

49,

50,

51 and

52

show mint and used issues in use from 1879 to 1896, although not in

complete sets. Colour variety is much improved, and some shades are

shown in the used sections.

Plate 49 (click to

enlarge)

A mint block of four of the 10 rupees issue with inverted watermark is

displayed on Plate 50. This is not listed in Barefoot,

as it normally does not include such varieties, except where it is

planned or consistent.

I illustrate another Supreme Court Statutory Declaration dated 14

January 1880 which comprises four pages. I have shown the first page on

Plate 53, but refrained from showing the rest. There is

a transcript of the whole document on

Plate 54.

Although it cannot readily be seen on the scan there are impressed Court

Duty stamps on each page of twelve cents. This compares with the

previous document on

Plate 45 of three pence per sheet,

therefore reflecting the change of currency. The declaration itself is

in many ways similar to the previous one where a Bill of Exchange was

dishonoured, although the actual Bill itself is not part of the exhibit.

The Chief Judge's signature (A G Ellis) is shown halfway down the front

page, and his initials appear also on the Internal Revenue stamp for

five rupees, a third of the way down on the left hand side: in addition

on the left there is a red Supreme Court wax seal. The adhesive stamp is

Barefoot #46 brown and purple (1879/96 issue).

It is worth observing the procedures used to secure further supplies of

revenue stamps when these were necessary. Communications between

Mauritius and the United Kingdom were virtually all by ship, and

therefore when the authorities wanted more supplies they had to order

well in advance.

Plate 55 shows a letter from the

Colonial Secretary's Office in Mauritius addressed to The Crown Agents

for the Colonies at Downing Street London S W, and dated 12 April 1884.

As will be seen readily, this is a copy of the original letter. Although

it is hand-written, the oval receipt handstamp of the Crown Agents has

been roughly sketched in by hand in pen and ink, and is dated 8 May 1884

; so it took four days less than a calendar month to reach London.

This letter, and the subsequent related documents, are all extracted

from the De La Rue archive books. Attached to the letter is a copy of

the actual requisition from the Mauritius General Post Office dated 7

April 1884 and shown on

Plate 56. I believe that the

red ink markings were added by De La Rue to complete their records. the

blue twenty-five cents Internal Revenue stamp is an original also, I

suspect, added by the printers.

Why are these only copies, one may ask? The final exhibit in this set of

three documents gives the answer.

Plate 57 shows again

a copy. This time it is a letter from De La Rue to the Crown Agents

returning the Requisition, and providing an estimate of the time which

would be taken to produce the printed item.

So one can calculate that at least three months was needed from start to

finish of the whole operation. This example also illustrates how

significantly technology has advanced over the past 100 years plus, in

matters of printing techniques, copying, email, air travel etc.

Continuing with the 1879/96 issues,

Plate 58 dated 20

June 1885, and described as Appendix A, is an original from the De La

Rue archives showing perforated plate proofs of the lower values, none

of which were adopted in this form. De La Rue tended at this time to use

the doubly fugitive colours of purple or green on many of their basic

proofs of lower values. These colours were sometimes used on the final

stamps, and are notable on some of the Great Britain stamps of about

this time. These colours were sensitive to light and/or water, and many

examples of bad fading exist, reducing values dramatically.

Appendix A is somewhat larger than A4 size paper, and I have had to

transfer a copy of the handstamped date from the top of the sheet, which

has been folded over, to he right hand side about an inch and a half

from the top.

Between 1885 and 1896, many provisional surcharges on previous issues of

Internal Revenue stamps. Some of the original material dates back to the

Sterling period of production. This was obviously a good and economical

way to use up old obsolete and/or surplus stock. One also suspects -

although I have no concrete evidence of this - that thoughts had already

started on the possibility of combining the use of stamps for both

postage and revenue purposes: thus there was some reticence in ordering

new issues. Plates

59 and

60 display some of the mint

and used (with shades) overprinted stamps.

These are not so easy to find, as is supported by Barefoot's catalogue

prices. However, a full listing is shown, together with all the other

Internal Revenue stamps later in this section.

Proceeding to 1897, on 21 April a requisition was sent to De La Rue from

the Crown Agents, together with a letter on the same page. This is shown

on Plate 61. The requisition covers not only Internal

Revenue items but also Bills of Exchange and Insurance stamps: the

letter itself only refers to the three Internal Revenue supplies

required, and specifies changed colours.

The Appendix on

Plate 62 compiled by De La Rue shows

these rather attractive colours, and was approved by the Crown Agents on

27 April 1897. This seems to indicate that the stamps were not produced

in 1896, as indicated in the Barefoot catalogue, but in the subsequent

year.

Continuing with the 1879/96 issues, I illustrate a piece cut from the De

La Rue archives (cut rather badly I am afraid) showing a request from

the Crown Agents for further quantities of the 50 cents and R2.50 stamps

in yellow and black and violet and black respectively. These are on

Plate 63 and it can be seen that both stamps are

denominated "fifty cents". They are imperforate. This item is also shown

in black and white in Ibbotson's book "The Postal History and Stamps of

Mauritius" page 86.

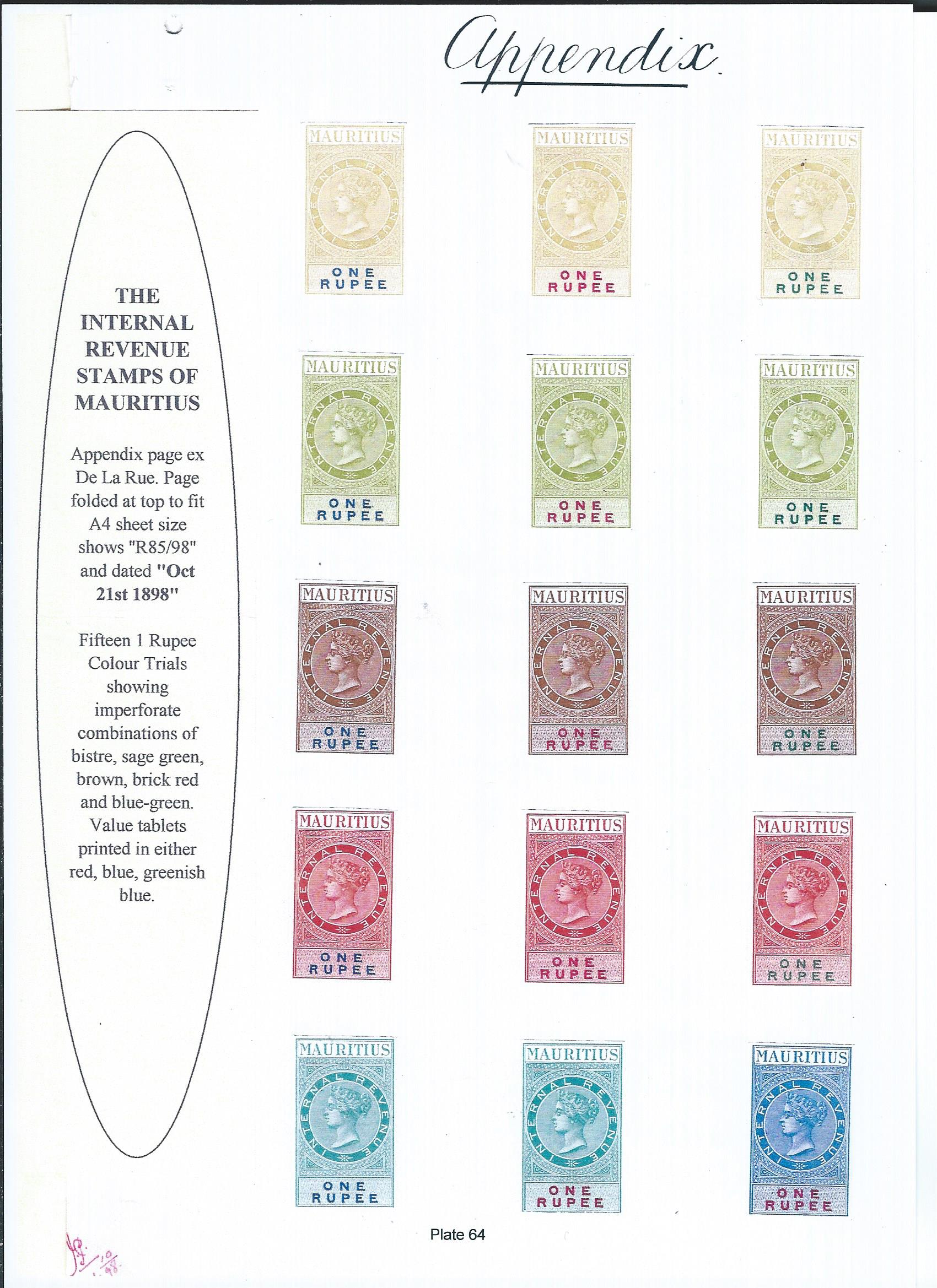

Why the printers were still issuing plate proofs as late as 21 October

1898 is not clear. Whether this was instigated by them, or it came as a

request from Mauritius or the Crown Agents is not known. Nevertheless,

this Appendix shown on

Plate 64 displays imperforate

combinations of bistre, brick red and blue-green. The one Rupee value

tablets are printed in red, blue or greenish-blue. None of these were

adopted.

Plate 64 (click to

enlarge)

Another example of an original die proof is shown on

Plate 65,

and again this was not adopted. It was originally dated by De La Rue 17

November 1898, and cancelled by the red diagonal line on 14 January

1899, when it was decided not to go ahead.

The following schedules give similar details to those shown under the

Bills of Exchange section, but it is worth mentioning (although in some

cases it is obvious) that the statistics shown for dates and quantities

of sheets issued are incomplete. This applies not only to items where

"Not known" is shown, but also it is likely to extend to other items as

well, as it cannot be certain that all issues have been discovered.

But I do feel that the statistics do give some help in ascertaining the

approximate rarity of one stamp as opposed to another. For example,

rather extreme I admit, if one totals up the number of sheets issued of

the 25 cents blue and blue cat #30 below, one arrives at a total of

6,814 sheets or 408,840 actual stamps at 60 stamps per sheet. Compare

this with the 40 sheets at #47 - 2,400 stamps, and the first exceeds the

second by more than 170 times!

Schedule of Internal Revenue Stamps Issued

| Barefoot Cat No |

Stamp Value and Colour | Date and Quantity of Sheets Issued |

| 1869/72 issue | ||

| 1 | 1d claret and blue | 29.01.1872 : 527 |

| 1a | 1d claret and blue (perf

12.5) Note: Ibbotson states "Exceptionally, this printing comprised sheets of 120 stamps instead of the normal 60" It could be that the perforation change listed by Barefoot was occasioned by the change in stamps per sheet, although I have no evidence of this. |

22.08.1876 : 148 |

| 2 | 2d blue and blue | Not known |

| 3 | 3d blue and blue | 29.01.1872 : 521 |

| 4 | 4d blue and blue | Not known |

| 5 | 6d blue and blue |

29.01.1872 : 1026 20.12.1873 : 1033 |

| 6 | 8d blue and blue | Not known |

| 7 | 1s brown and purple |

29.01.1872 : 519 20.12.1873 : 1023 |

| 8 | 2s brown and purple | 29.01.1872 : 259 20.12.1873 : 1025 |

| 9 | 3s brown and purple | Not known |

| 10 | 4s brown and purple | Not known |

| 11 | 5s brown and purple | Not known |

| 12 | 10s brown and purple | Not known |

| 13 | £1 mauve and brown | Not known |

| 1874 issue | ||

| 14 | 14 6d blue and blue | Not known |

| 15 | 15 1s brown and purple | Not known |

| 16 | 16 2s brown and purple | Not known |

| 1878/79 issue

(new currency) Figures and words |

||

| 17 | 5c red and blue | 07.10.1877 : 243 20.03.1877 : 238 |

| 18 | 15c blue and blue | 07.10.1877 : 404 20.03.1877 : 404 |

| 19 | 25c blue and blue | 07.10.1877 : 1018 20.03.1878 : 986 |

| 20 | 50c brown and blue | 07.10.1877 : 502 20.03.1878 : 494 |

| 21 | 1r brown and purple | 07.10.1877 : 416 20.03.1878 : 398 |

| 22 | 1r50c brown and purple | 07.10.1877 : 103 |

| 23 | 2r brown and purple | 07.10.1877 : 74 20.03.1878 : 74 |

| 24 | 2r50c brown and purple | 07.10.1877 : 85 20.03.1878 : 78 |

| 25 | 5r brown and purple | 07.10.1877 : 55 20.03.1878 : 56 |

| 26 | 10r brown and purple | 07.10.1877 : 28 20.03.1878 : 26 |

| 1879/96 issue

as above but value in words |

||

| 27 | 5c red and blue | 27.04.1881 : 550 03.10.1884 : 250 30.07.1885 : 253 |

| 27a | 5c red and blue-black | 10.05.1886 : 500 16.08.1894 : 102 06.03.1895 : 1024 24.08.1900 : 200 18.09.1901 : 400 |

| 28 | 15c blue and blue | 11.08.1890 : 96 06.10.1891 : 103 04.04.1892 : 92 16.08.1894 : 102 25.06.1896 : 72 |

| 29 | 15c grey and black | 24.07.1897 : 204 |

| 30 | 25c blue and blue | 06.01.1883 : 402 05.06.1884 : 817 30.07.1885 : 608 10.05.1886 : 1010 24.07.1888 : 402 23.03.1891 : 253 06.10.1891 : 410 04.04.1892 : 400 20.07.1893 : 402 16.10.1894 : 400 06.03.1895 : 510 08.05.1896 : 500 30.04.1900 : 300 18.09.1901 : 400 |

| 31 | 50c blue and blue | 06.01.1883 : 203 03.10.1884 : 240 30.07.1885 : 410 04.04.1892 : 100 21.03.1893 : 85 30.12.1893 : 150 16.10.1894 : 305 |

| 32 | 50c yellow and black | 25.01.1898 : 506 16.01.1899 : 172 24.08.1900 : 150 18.09.1901 : 300 |

| 33 | 75c green and black | 06.11.1878 : 205 30.12.1893 : 102 06.03.1895 ; 102 |

| 34 | 1r brown and purple Note: No details are available of when #34 was changed to #35. The printings have therefore been shown under one heading for both issues. |

28.02.1884 : 96 |

| 35 | 1r brown and red | 30.07.1885 : 200 10.05.1886 : 250 06.10.1891 : 92 04.04.1892 : 92 30.12.1893 : 146 16.10.1894 : 203 08.05.1896 : 122 |

| 36 | 1r red and black | 14.07.1897 : 202 18.09.1901 : 60 |

| 37 | 1r25c red and black | 06.11.1878 : 152 30.12.1893 : 104 |

| 38 | 1r50c brown and purple | 30.12.1893 : 104 |

| 39 | 1r85c red and black | 06.11.1878 : 100 30.12.1893 : 100 |

| 40 | 2r brown and purple | 27.07.1882 : 103 03.10.1884 : 60 30.12 1893 : 104 |

| 41 | 2r green and black | 14.07.1897 : 100 |

| 42 | 2r50c brown and purple | Not known |

| 43 | 2r50 violet and black | Not known |

| 44 | 3r brown and blue | 16.01.1899 : 86 |

| 45 | 3r75c brown and black | 06.11.1878 : 52 |

| 46 | 5r brown and purple | 27.07.1882 : 86 10.05.1886 : 58 |

| 47 | 5r orange and purple | 16.01.1899 : 18 06.08.1901 : 22 |

| 48 | 7r50c grey and black | 06.11.1878 : 52 |

| 49 | 10r purple and brown | 27.07.1882 : 22 11.08.1890 : 12 03.09.1895 : 17 16.01.1899 : 18 06.08.1901 : 22 |

| Because all of the rest of this listing comprises overprinted surcharges of Internal Revenue stamps already produced, and hopefully recorded above, I merely list catalogue numbers and descriptions for the sake of completion in showing the whole of the Barefoot categories. | ||

| 1885/94 issue Provisional Surcharges |

||

| 50 | 15c on 4s | |

| 51 | 25c on 3d | |

| 52 | 25c on 6d | |

| 1886/94 issue Further Provisional Surcharges |

||

| 53 | 5c on 75c | |

| 54 | 15c on 1s | |

| 55 | 15c on 1r50c | |

| 56 | 25c on 6d | |

| 57 | 25c on 15c | |

| 58 | 25c on 75c | |

| 58a | 25c on 75c (dropped "c") | |

| 59 | 25c on 1r25c | |

| 60 | 25c on 1r50c | |

| 61 | 25c on 1r85c | |

| 62 | 25c on 1s | |

| 63 | 1r on 1r25c | |

| 64 | 1r on 2s | |

| 65 | 1r on 3s | |

| 66 | 1r on 4s | |

| 67 | 1r on 5s | |

Again, as with other Revenue stamps, the cancels are worthy of examination and collection. In analysing these, even more are indistinct than those on the Bills of Exchange material, although stronger magnification and assiduous application may decipher more than I have able to achieve. I have found the following firms etc:

-

B B & Co (Blyth Bros)

-

B B & Co (Perfin)

-

Bank of Mauritius

-

Elias Mallad & Co

-

Hajeew Hamode Ahoo & Co

-

Joosop Jacob

-

Manuscript cancels with signatures/initials/dates

-

Mauritius Commercial Bank

-

Mauritius First Insurance Company

-

New Oriental Bank Corporation

-

Oriental Bank Corporation

Undoubtedly, merchants are rarer than banks. This

somewhat surprises me, in view if the breadth of uses to which the

Internal Revenue stamps could be put. This may be because banks - and

possibly insurance companies - tended to keep their records better and

longer.

Another offshoot of study could well be to research products or

serviceshich, by Enactment of Parliament (either locally or in the

earlier days by the U K), were exempted from any or some form of duty.

One example of this is contained in the Mauritius Sugar Syndicate Act of

1951 which, inter alia, states:-

"8. Exemption from Duty

All sales of sugar made........ shall be free from stamp and other

duties except stamp duty on receipts, and shall be exempt from

registration."

This was obviously done to boost the declining sugar trade from the

island, but there could be other items within the Mauritius or British

Colonial legislation which showed special attention either to an

enhanced, decreased, or exempt level of taxation.